What Is Accounting for Nonprofit Organizations: Get the inside scoop on how nonprofits should account for stock, assets, and compliance in field. This introduction to nonprofit accounting will cover what kind of reporting is most helpful for donors, how to best manage your budget, and how to report information about donations.

Accounting for Nonprofit Organizations provides basic financial accounting and reporting requirements that are specific to nonprofits. This introductory level book fills a gap in the literature, bridging the gap between general-purpose textbooks and voluminous pronouncements on individual standards. It explains how accounting for nonprofits is no different from accounting for for-profit organizations, but with some additional considerations for reporting to stakeholders including other nonprofit organizations, government agencies, grantors, financial contributors, and clients.

What is Nonprofit Accounting?

Nonprofit accounting is the unique process by which nonprofits plan, record, and report upon their finances. While for-profits primarily focus on earning a profit, nonprofits focus more on the accountability aspect of accounting. They follow a specific set of rules and procedures that help them stay accountable to their donors and contributors.

In the rest of this article, we’ll cover the basics and best practices that all nonprofit professionals should know about accounting. Understanding the basics will help you better manage and plan your programs in a way that brings the most value from your finances.

Basics and Best Practices of Nonprofit Accounting:

- How Nonprofit Accounting is Different

- Nonprofit Accounting Statements and Reports

- Best Practices for Nonprofit Accounting

- To Hire or Outsource for Nonprofit Accounting

- Our Nonprofit Accounting Recommendations

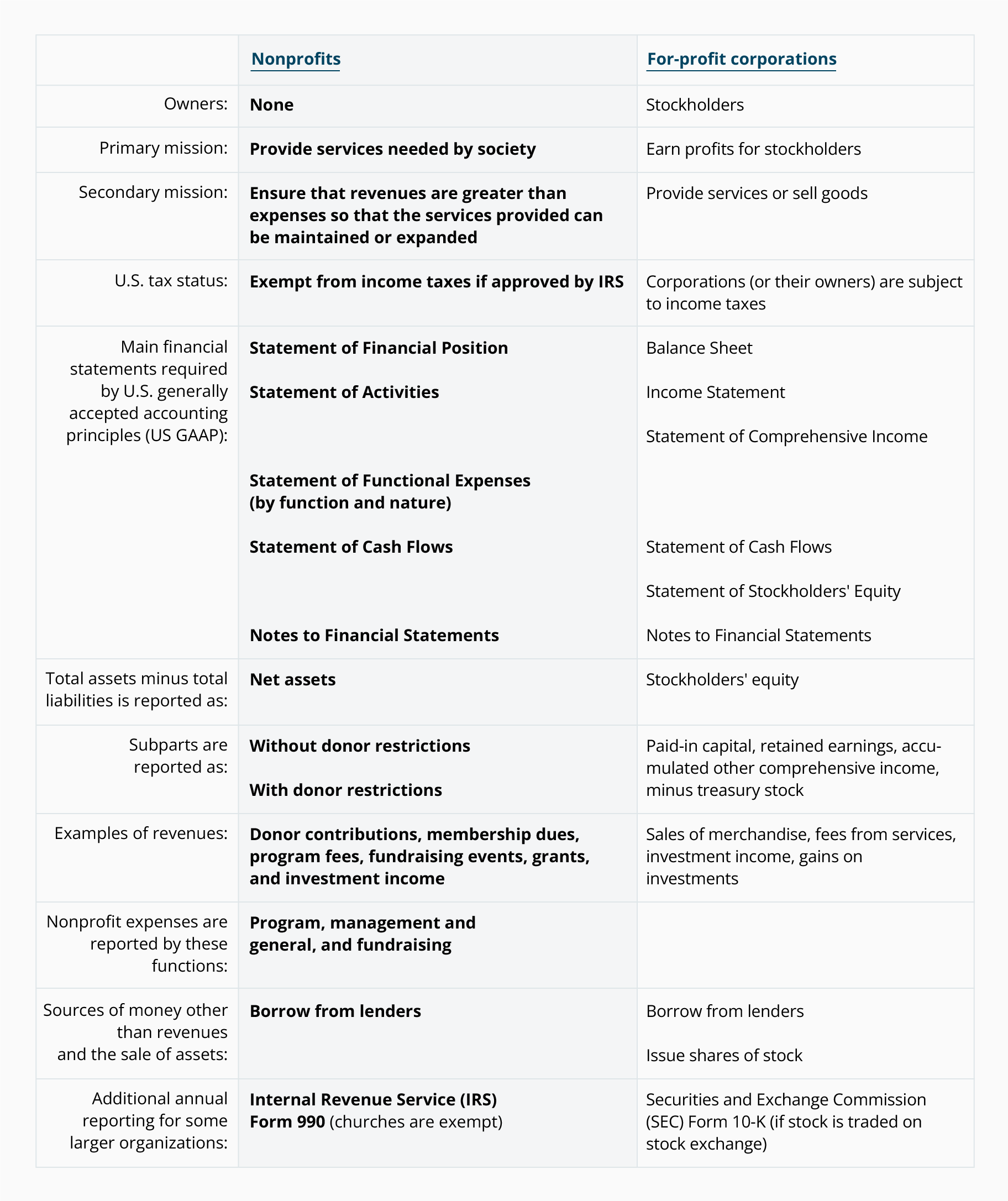

Nonprofits vs. For-Profit Corporations

The following table highlights some of the key differences between nonprofit organizations and for-profit corporations:

Mission and Ownership, Tax-Exempt Status

Mission and Ownership

While businesses are organized to generate profits, nonprofits are organized to address needs in society. As a result, nonprofits will issue a statement of activities instead of the income statement issued by for-profit businesses.

Since nonprofits do not have owners, there is no owner’s equity or stockholders’ equity and therefore no distributions to owners.

Some people mistakenly assume that if an organization is designated as a nonprofit, it cannot legally earn profits. In fact, having revenues in excess of expenses is almost a necessity for a nonprofit if it hopes to withstand such things as:

- unexpected expenses

- uneven flows of revenues

- a decrease in revenues

- rising costs due to inflation

- an increase in staffing needs

- an increase in the need for its services

- the purchase or replacement of needed equipment

- other needs since a nonprofit cannot issue shares of stock

Tax-Exempt Status

Nonprofit organizations may apply to the Internal Revenue Service in order to be exempt from federal income taxes.

A second issue is whether a donor’s contribution to a nonprofit organization will qualify as a charitable deduction on the donor’s income tax return. For example, churches, schools, and Red Cross chapters are some of the nonprofits that will qualify as tax-exempt and their donors’ contributions will also qualify as charitable deductions on the donors’ income tax returns.

However, there are nonprofits that qualify as tax-exempt but their donors’ contributions do not qualify as charitable deductions (although they may qualify as business expenses). Examples of these nonprofits include social organizations, chambers of commerce, college fraternities and sororities, amateur sports clubs, employee organizations, and more.

You can learn more about the tax-exempt status for a nonprofit, the deductibility of contributions by donors, and the taxability of activities not directly related to a nonprofit’s exempt purpose in the Internal Revenue Service Publication 557, Tax-Exempt Status for Your Organization, which is available at no cost on IRS.gov.

Even if a nonprofit is exempt from federal income taxes, it is likely that its employees will be subject to employment taxes. Nonprofits may or may not be exempt from sales taxes, real estate taxes, and other taxes depending on which state in the U.S. they are incorporated or operate.

Nonprofit accounting

Whether you’re thinking about starting a nonprofit or already have, understanding the unique aspects of accounting for nonprofit organizations is essential.

1. Choose an accounting method

Like for-profit businesses, nonprofit bookkeeping relies on choosing an accounting method to record incoming and outgoing money.

Like any business, your nonprofit needs a healthy cash flow to run. You need to earn enough money to pay things like employee wages, unexpected expenses, utility bills, rent, etc.

Although you might not sell products like the typical business, you have many sources of revenue. You might have members who pay dues or donors who contribute money. And, you may host fundraising events to bring in revenue.

You must record all incoming revenue and outgoing payments with an organized accounting system. You can choose a cash-basis or an accrual accounting system for nonprofit organization.

Cash-basis accounting is a system where you record expenses or income when you actually pay or receive them, not when the transaction takes place. For example, you run a nonprofit where members must pay dues. Using the cash-basis accounting system, you record payment when you actually receive dues from members. However, you cannot use this method if you make more than $5 million in annual gross sales or more than $1 million in gross receipts for inventory sales, or if you extend credit.

Accrual accounting is when you record transactions when they actually take place. This method uses a double-entry bookkeeping system. If your nonprofit collects membership dues, you would record income when you send the invoice, even though you haven’t physically received money.

2. Understand tax responsibilities

If you apply and qualify for tax-exempt status, you do not need to pay federal income taxes. And, you might also be exempt from sales and property taxes if you have tax-exempt status.

You must apply for tax-exempt status by filing Form 1023, Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code. Then, the IRS will decide if you qualify based on whether you are a “charitable” organization.

Being exempt from federal income taxes does not necessarily exempt you from filing an annual small business tax return. You are still required to report revenue and expenses to the IRS. Keep accurate records of and report your activities and finances for the year.

Unless you are not required to file a return (e.g., a church), you must file Form 990, Return of Organization Exempt from Income Tax or Form 990-EZ. Your form is due on the 15th day of the fifth month after your accounting period ends.

3. Create the appropriate financial statements

In nonprofit accounting, you should create financial statements to report your business’s finances.

For-profit businesses use three main financial statements, which are income statements, balance sheets, and cash flow statements. Nonprofit businesses use similar financial statements, but they have different names and are organized differently.

Nonprofit accounting relies on using the statement of financial position (balance sheet), statement of activities (income statement), and cash flow statement.

The statement of financial position gives you a screenshot of the health of your nonprofit during a period of time. The statement shows your assets, liabilities, and net assets. Unlike the balance sheet, the nonprofit version substitutes net assets for equity. Your net assets plus liabilities must equal your assets on the statement of financial position.

Net assets are classified in one of two ways: with donor restrictions or without donor restrictions. If donors make donations for specific purposes, you must label them as “with donor restrictions.”

Here is an example statement of financial position:

The statement of activities works similarly to the income statement. Its purpose is to report revenue and expenses during a period of time. Like the statement of financial position, you must report revenues with or without donor restrictions.

Here is an example statement of activities:

Lastly, the cash flow statement shows you how much money is entering and leaving your organization during a specific time period. The cash flow statement organizes cash into three categories, which are operating, investing, and financing activities. You can have either positive or negative cash flow in your nonprofit.

Take a look at this cash flow statement example:

Conclusion

What is accounting for nonprofit organizations? Nonprofit organizations are engaged in charitable, educational, religious, or literary pursuits. In general, the purpose of a nonprofit organization is to fulfill needs; therefore, it can be assumed that only revenues go into the income statement.