In financial statement analysis, different tools are employed to analyze the data. These tools can be divided into three categories: primary financial statements, secondary financial statements; and analytical tools. The primary financial statements consist of a corporation’s balance sheet, which provides information about a firm’s assets, debt and equity, and income statement, which details a company’s revenue and expenses over a period of time.

If you’re new to business, you may have no idea what a “tool” is. But if you are familiar with tools, this article will help you understand why they are used in financial analysis and how they can help your company grow.

Common-size Analysis

The common-size analysis involves creation of a ratio between each financial statement item and a base item. This, typically, translates to total assets (when common-sizing the balance sheet) or total revenue (when common-sizing the income statement).

The vertical common-size analysis highlights the composition of the balance sheet and helps to answer questions such as what mix of assets the company is using, how it is financing itself, and how its balance sheet composition compares with that of its peers. Finally, the vertical common-size analysis offers reasons behind the differences that may exist among companies in the same industry and environment.

Horizontal common-size analysis can highlight structural changes that have occurred in a company over time. An analysis of past trends (historical analysis) can help to develop future expectations by evaluating whether trends are likely to remain constant or change.

Trend analysis provides useful information on a company’s historical performance and growth. It can be used as a planning and forecasting tool for management and analysts.

Cross-sectional analysis or relative analysis compares metrics for one company with the same metrics for another company. This allows comparisons to be made irrespective of whether or not the companies are of significantly different sizes and/or report financial data in different currencies.

Whenever companies whose financial performance is being compared differ significantly in regard to size and/or the currency in which their finacial data is reported, a comparison of their net income as reported will not be useful. Financial ratios and common-size financial statements can remove size as a factor and enable a more feasible comparison. Additionally, in addressing the challenge of data being reported in different currencies:

- all reported amounts may be translated into one common currency using the foreign exchange rates at the end of a period; or

- all reported amounts may be translated into one common currency using the average foreign exchange rates during the period; or

- comparability is possible without the translation of currencies if ratio analysis is the primary focus.

The reported nominal currency revenue or net income amounts for a company may not highlight significant changes in its performance over time. However, using ratio analysis, charts, or stating financial statement quantities relative to a selected base year value, can make these changes more visible and apparent.

Differences in fiscal year ends can pose a challenge to comparability. This can be overcome by using the trailing twelve months of data.

Differences in accounting standards can also limit comparability. A financial analyst should, however, seek to identify where these differences lie and the impact they may have on comparability. As best as possible, this impact should be minimized by making adjustments where feasible.

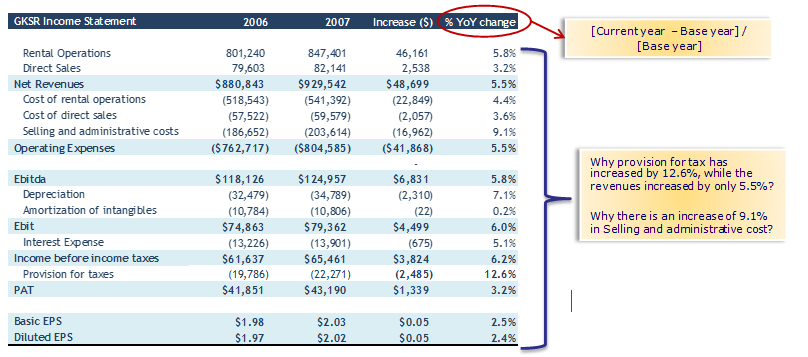

Comparative Income Statement

Three important pieces of information are obtained from the Comparative Income Statement. They are Gross Profit, Operating Profit, and Net Profit. The changes or the improvement in the profitability of the business concern is found out over a period of time. If the changes or improvement is not satisfactory, the management can find out the reasons for it and some corrective action can be taken.

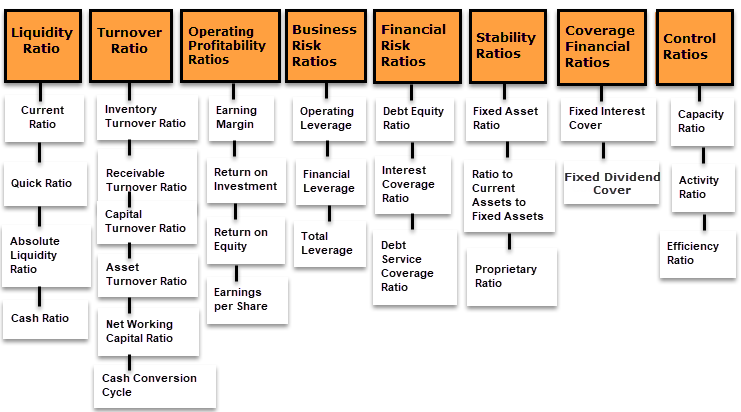

Ratio Analysis

Ratio Analysis is the most commonly used financial analysis tool used in the market by an analyst, experts, internal Financial Planning & Analysis department, and other stakeholders. Ratio Analysis has various kinds of ratios, which can help in commenting on

- Profitability Ratio Formula

- Rate of Return Analysis

- Solvency Ratios

- Liquidity

- Coverage of Interest or any cost

- Comparing any component with turnover

Moreover, an entity based on their requirement can prepare the ratios for their analysis and try to manage the operations.

However, below are the odd side of ratio analysis:

- Highly relying on past information

- Inflation impact is ignored

- Chances of manipulation/window dressing of financials, which can enhance the fairness of ratios

- Any seasonal changes, based on the nature of business will be ignored, as it cannot be directly adjusted in financials

Comparative Statements

Comparative statements deal with the comparison of different items of the Profit and Loss Account and Balance Sheets of two or more periods. Separate comparative statements are prepared for Profit and Loss Account as Comparative Income Statement and for Balance Sheets.

As a rule, any financial statement can be presented in the form of a comparative statement such as comparative balance sheet, comparative profit and loss account, comparative cost of production statement, comparative statement of working capital, and the like.

Regression Analysis

Regression analysis helps to identify relationships between variables which can lead to forecast estimates. It can also facilitate the identification of items or ratios that are moving contrary to their historical statistical relationships.

Comparative Balance Sheet

The financial condition of the business concern can be find out by preparing comparative balance sheet. The various items of Balance sheet for two different periods are used. The assets are classified as current assets and fixed assets for comparison. Likewise, the liabilities are classified as current liabilities, long term liabilities and shareholders’ net worth. The term shareholders’ net worth includes Equity Share Capital, Preference Share Capital, Reserves and Surplus and the like

Benchmarking

Benchmarking is the process of comparing the actuals with the targets set out by the top management. Benchmarking also refers to the comparison made with the best practices and strives to achieve the same, keeping the same as the target. In benchmarking below steps are to be performed:

- Step 1: Select the area which is needed to be optimized.

- Step 2: Identify the trigger points with which it can be compared.

- Step 3: Try to set up the better standard for the same or take industrial standards as the benchmark.

- Step 4: Evaluate the periodic performance and measure the trigger points.

- Step 5: Check whether the same is achieved or not; if not, do variance analysis.

- Step 6: If achieved, then strive to set up the better benchmark.

For doing the above benchmarking, ratios, operating margin matrix, etc. can be used. The operating margin of the industry average can be compared and should try to arrive at a better position. The company named Xerox, to sustain itself in the photocopy business, initiated Benchmarking. Presently, they have optimized more than 100 functions in comparison to industrial standards. Benchmarking can be observed as a tool for improvement with the aim of customer-focused improvement activities and should be driven by customer and internal organization needs. Benchmarking is the practice of being humble enough to admit that someone else is better at something and wise enough to learn how to match and even surpass them.

Average Analysis

Whenever, the trend ratios are calculated for a business concern, such ratios are compared with industry average. These both trends can be presented on the graph paper also in the shape of curves. This presentation of facts in the shape of pictures makes the analysis and comparison more comprehensive and impressive.

Comparative Financial Statement

Comparative financial statements are used in horizontal analysis or trend analysis. It helps in analyzing the periodic change in various components of the financial statements and displays which component has the maximum impact.

Such comparative financial statements can be either prepared in currency amount terms or percentage terms.

Thus from the above, one can easily compare the periodic data either in numeric format or in percentage terms.

The comparative financial statement has advantages like easy comparability, observing the trend, periodic performance evaluation, etc. However, it has disadvantages like ignoring inflationary impact, high dependability on financial information, which can be manipulated, a different method of accounting used by various entities, etc.

Statement of Changes in Working Capital

The extent of the increase or decrease in working capital is identified by preparing the statement of changes in working capital. The amount of net working capital is calculated by subtracting the sum of current liabilities from the sum of current assets. It does not detail the reasons for changes in working capital.

Cost Volume Profit Analysis

This analysis discloses the prevailing relationship between sales, cost, and profit. The cost is divided into two. They are fixed costs and variable costs. There is a constant relationship between sales and variable costs. Cost analysis enables the management to better profit plans.

Accounts receivable

Accounts receivable are the amounts of money that customers owe you. It is important to understand that accounts receivable does not mean cash in your hand, but rather an asset on your balance sheet. Accounts receivable represents money earned in the past but not yet received. This means that it is an asset because it will be converted into cash at some point in the future and also a liability because you owe someone else money for services or goods already provided.

Liquidity ratios

You’ll also want to know about liquidity ratios, which measure a company’s ability to pay its bills. These ratios are useful for comparing companies, or for comparing a company to industry standards.

Accounts payable is the amount owed to suppliers and usually takes the form of checks that haven’t been cashed yet. In order for a business to keep running smoothly and avoid cash flow problems, it needs enough money on hand in case there aren’t any funds available from banks or credit lines.

You’ll want to learn about current ratios, quick ratios and cash flow ratios before starting your financial analysis training course because these tools will be very helpful when analyzing companies’ financial statements later on down the road! If you’re looking at industry averages or historical numbers instead of today’s figures then this might not apply so much but still relevant nonetheless so check them out!

Gross profit

Gross profit is the difference between total revenue and total cost of goods sold. Gross profit is a measure of profitability, and it’s important because it helps you determine how much money your company’s products or services are earning before deducting costs such as labor, overhead, taxes and interest payments.

Gross margin is calculated by dividing gross profit by revenue. Net income is the money your business earns after paying expenses — including salaries for employees as well as any interest on debt incurred by the company during its operations (and before paying out dividends). Net income is also used to calculate gross profit; this way you can see how much cash flow your business will have before deducting those extra costs.

Cash flow

Cash flow is the net amount of cash and cash equivalents that a company receives from its operations. For example, if a company receives $100 in revenue but has to pay $100 worth of expenses, its cash flow would be $0.

The difference between cash flow and earnings is that earnings reflect profits after deducting costs such as depreciation and interest expenses. Cash flow accounts for all incoming funds regardless of whether they are directly related to generating profits or not (e.g., sales discounts).

A business can generate positive or negative cash flows depending on how well it manages its assets and liabilities during a given period. For example, if a company pays only half of what it owes at the end of each month because it doesn’t have enough money in its checking account, then this means that every dollar earned by selling products will result in two dollars being spent immediately before they can be recorded as income on the balance sheet.

Cash flow is important because it shows how much cash a company has available to pay off debtors or make investments into new projects without having to borrow more money from creditors (or investors) first

Contingent liabilities

- A contingent liability is a potential future obligation that may or may not be incurred. It includes lawsuits, environmental liabilities and warranty obligations.

- These items are not recorded on the balance sheet until they are actually incurred by a company.

- They often cannot be known for certain when recording them on the balance sheet, which increases uncertainty and makes it difficult to estimate their value.

- Liquidity ratios measure a company’s ability to pay off its debts and meet its financial obligations as they come due. The two most common liquidity ratios are the current ratio and acid test (quick) ratio.

Balance sheet

The balance sheet is a snapshot of a company at a specific point in time. It shows the assets, liabilities and equity of the business. The balance sheet can help you understand if your business is running at a profit or loss, because it will show whether your current assets are greater than your liabilities. Comparing past balance sheets will also allow you to see how your business has changed over time.

The most important section on any financial statement is usually the income statement, but sometimes it’s necessary to look at other statements as well. For example, if you want to know how much money is coming into or leaving an organization (such as when analyzing cash flow), then looking at cash flows from operating activities on an income statement may not be enough; instead it might be more useful for investors who are primarily interested in how much cash each month goes back out into their pockets!

Inventory turnover ratio

- Inventory turnover ratio. The inventory turnover ratio is a way to measure how fast you sell your inventory. It’s calculated by dividing the cost of goods sold by your average inventory for a certain period (normally one year). A higher number means that you sell more products per year, which is good because it means that people are buying what they need from you and not just sitting on it in storage.

- Gross profit margin. Gross profit margin measures how efficient you are at producing products that people want, without having to count overhead expenses like rent or utilities into the equation. This number is important because it helps determine whether or not your company can make money—if gross profit sales exceed total costs required to make those sales, then there will be money left over after all expenses have been paid off; otherwise there won’t be any profits left over at all! You’ll also use this information when calculating net income later on down below….

Working capital efficiency ratio

The working capital efficiency ratio measures a company’s ability to generate cash from its operations. It is derived by dividing current assets by current liabilities. A high ratio means that the company has more cash on hand than it owes in bills, which indicates strength and financial health. A low ratio could mean that you are having trouble paying your bills with what you make from business operations, or it could indicate that you have too much inventory on hand (you should try to have as little inventory as possible).

Understanding these tools can help you understand what is going on in your business.

If you’re taking a class on financial analysis, chances are that one of the tools you’ll be learning about is the balance sheet. This tool shows the assets and liabilities of a business at a particular moment in time. You can use it to see where your money comes from, how much cash you have on hand, what kinds of investments you have made, who owes the most money to whom (your debtors), and more.

The income statement is another common financial analysis tool. It tracks all of the revenue generated by your business over time—and all expenses incurred as well. By comparing these numbers over time or between companies with similar operations and objectives, you can get an idea of whether there are areas where improvement might be needed or opportunities for improvement exist; this information can help guide planning decisions going forward so that when things change in your industry—which they inevitably will—you’ll be able to adapt quickly enough not only survive but thrive as well!

Conclusion

There are numerous tools available in the market to carry out financial analysis based on various needs. Organizations, based on their needs, also build up various in-house tools, which help them to track their requirements. In today’s competitive world, it is of utmost importance to track the performance of its organization, as well as of its competitors, as it will help in maintaining the performance and help in thriving the business.